Wealth Transfer Newsletter November 2010

In this issue:

- Current Developments

- Transfers to GST Exempt Trusts in 2010

- "Top Ten" Things You May Not Be Doing, But Should Consider

- Planning Opportunities in a Favorable Interest Rate Environment

- Team Accomplishments and Accolades

Greeting

As we send this newsletter the election results are reasonably certain but the impact of the changes in the make up of Congress does not clear up the tax and planning uncertainties. It has been a remarkable year of transition with no estate or generation skipping transfer tax, and there are many opportunities that we believe are available uniquely that will end on December 31, 2010.

We would suggest that you particularly pay attention to the immediate 2010 planning ideas and our "Top 10" Planning Ideas for 2010 and beyond included in this newsletter. Since there are many traps for the unwary in any planning that is implemented, you should work closely with your advisors to avoid them. For clients who want to make substantial gifts in 2010 or gifts to or for the benefit of grandchildren, since there is no GST tax in 2010, planning with advisors is particularly important. The Roth conversion for qualified plans and IRA’s, which for many should be made in 2010 instead of in subsequent years, also needs to be addressed as quickly as possible. Clients should prepare now for the real possibility that the estate tax may be increased in terms of rates returning to 55% and a reduction of exemption from federal estate tax to $1,000,000 if there is post-election gridlock on estate and gift tax legislation.

We here at Moore & Van Allen certainly stand ready to assist with any actions required to implement planning prior to year end. We also will try to keep you abreast as soon as clarity is achieved in any of the areas. We do expect formal guidance from the Treasury before year end on a number of matters, so much of the proposed planning needs to be put in place now, but subject to completion and delivery later in December after guidance is issued and any new legislation is taken into consideration.

I want to congratulate all of those in our Moore & Van Allen Wealth Transfer Group with the recognition that they have received from many sources on many occasions for their pro bono contributions and their participation in the education of other professionals in the wealth transfer planning area. With change in the air, both politically and economically, 2010 year-end planning may be more important than any prior year in the past decade.

![]()

Current Developments

Planning Opportunities and Updates

With our newsletter, Moore & Van Allen would like to keep you apprised of the most recent trends in tax and estate planning. In recent years, and as noted in past newsletters, we have witnessed substantial changes in the estate, gift and generation-skipping transfer (GST) tax laws both on the federal and state levels. However, just as important, we have also witnessed a number of significant changes with respect to the non-tax elements of estate planning. Accordingly, we thought that it would be appropriate to summarize a number of planning ideas that you may wish to consider. Also, if it has been some time since you revisited your estate plan, we strongly encourage you to contact one of our team attorneys to discuss a review and potential update of your estate plan to reflect these and other planning ideas.

Asset Protection for Descendants

Given the unfortunate frequency of divorces and increased litigation, you may want to consider the use of trusts to help protect the assets passing to descendants during lifetime or at death. Traditionally, assuming a child was responsible and old enough to receive an inheritance, the child typically received his or her inheritance “outright” and not in trust. As a result, many children who inherited assets then mixed the inherited assets with those of his or her spouse, including buying homes together and investing using a joint account, making it difficult or impossible to separate out upon divorce the inherited assets from assets earned during the marriage. The practical result of this is that parents have ended up benefitting persons and new families that they had no intention of benefitting when inherited assets ended up with the divorcing spouse. Most parents are comfortable with the spouses of their children having a higher standard of living as a result of family wealth. However, in contrast, most families do not want to benefit a spouse that is divorcing his or her child. Furthermore, inherited assets in a child’s name are also exposed to judgments resulting, for example, from car accidents, bad business deals, worker injuries on the child’s property, and poor spending decisions.

In recent years, the use of trusts to help protect those assets has become much more common, often because of state laws that make it clear that a creditor cannot force assets out of a trust, assuming the trust has been properly drafted and administered. Furthermore, in many states, the child can even serve as Trustee of his or her own trust and still retain a much higher degree of asset protection than if those assets were in the child’s own name. We should note that many of these same protections are also available for trusts for the benefit of a surviving spouse. Additionally, you may want to consider asset protection planning for yourself.

Increased Trustee Guidance

When structuring a trust for a child or other descendant, perhaps the most critical decision is the selection of an appropriate Trustee, because the Trustee is responsible for not only determining how trust assets are invested, but also for deciding on the distributions to beneficiaries as authorized by the trust.

Traditionally, trusts have been drafted to allow distributions for a beneficiary’s “health, education, support and maintenance.” While appropriate distributions for “health” (e.g., health insurance and medical bills) and education (e.g., tuition, room and board, and books) are fairly easily determined, the terms “support” and “maintenance” could mean simply the supplementation of a basic lifestyle or on the other extreme, the provision of a luxurious lifestyle without effort on the part of a beneficiary.

Accordingly, in recent years with increased litigation by beneficiaries to obtain distributions from trusts, more recent trusts have granted more flexibility and discretion to the Trustees, so that a Trustee is not forced to make distributions for particular items and instead may make distributions in the Trustee’s sole discretion.

Additionally, some clients, particularly clients with minor descendants, are taking the time to better express their wishes in the form of a “Trustee Guidance Letter,” so that both the Trustee and the beneficiary have a clear understanding of the parent’s or grandparent’s wishes. Common issues addressed in such a document include (1) a beneficiary being responsible and a productive part of society, (2) the importance of education, (3) making provision for a beneficiary’s medical and health insurance needs, (4) preventing beneficiaries from “living off” of trusts, (5) avoidance of trust distributions which enable a drug or alcohol addiction, and (6) providing examples of appropriate and inappropriate distributions. While these issues can be addressed in a mandatory way, they are often stated in terms of recommendations instead to provide for maximum flexibility.

Modification and Decanting of Trusts and the Use of Trustee Amendment Provisions

Given continuing changes in society, tax law, client’s wishes, beneficiary situations, and estate planning strategies, many states have passed laws which allow for the modification of irrevocable trusts or the transfer of assets from an existing irrevocable trust to a new trust by “decanting” the trust. Accordingly, if you created or are the beneficiary of an irrevocable trust, you should consider asking that an attorney at Moore & Van Allen review the trust to determine whether one of these options could and should be used.

As examples, clients often determine that (1) a successor Trustee that is named in the document is no longer appropriate, (2) the right to remove a corporate Trustee is not provided for and should be included, or (3) the distributive provisions of the trust should be updated. In certain cases, assuming the grantor (i.e., the person who created the trust) and the beneficiaries consent, the modification can be done without court approval. A related trend in estate planning is the inclusion of trustee amendment provisions, so the types of changes discussed above can be made more simply by the Trustee without court approval and regardless of whether the grantor of the trust is living.

In coming newsletters, we will highlight additional planning ideas that you may want to consider for inclusion in your estate plan. However, in the interim, please feel free to contact one of the team’s attorneys to discuss your planning and how these ideas can benefit your particular situation.

Transfers to GST Exempt Trusts in 2010

With the current absence of the Generation-Skipping Transfer (“GST”) tax in 2010, outright generation-skipping transfers made this year will not be subject to GST Tax. However, transfers to a GST Exempt Trust such as an Irrevocable Life Insurance Trust (“ILIT”) or Dynasty Trust (whether or not an ILIT) may result in future taxable distributions or terminations in 2011 or subsequent years as there is no procedure for the allocation of GST exemption to transfers made during 2010. Without the ability to allocate GST exemption, the ILIT could effectively no longer be entirely GST exempt. As such, it may not be advisable to risk creating a trust with both GST exempt and non-exempt assets by gifting assets to an ILIT in 2010. To minimize the risk in the ILIT context, clients should consider either borrowing against trust assets or making loans to ILITs to fund 2010 life insurance premiums. Treasury guidance is expected on this issue prior to year-end. With respect to the use of Dynasty Trusts that are not ILITs and may be grantor or non-grantor trusts, barring Treasury guidance, the gifts in 2011 may need to be made outright directly to grandchildren, possibly in the form of interest in a limited liability company or limited partnership, particularly where the grandchildren are minors.

"Top Ten" Things You May Not Be Doing, But Should Consider

In the current landscape of uncertainties peppering the future of the federal estate and gift tax, a number of simple but true techniques are still available to transfer assets to beneficiaries. Following are a list of ten things that savvy taxpayers, if not already doing so, should consider:

1. Create medical and tuition payment accounts. In general, Section 2503(e) of the Internal Revenue Code (the “Code”) allows taxpayers an unlimited gift tax exclusion for amounts paid on behalf of any donee, directly (1) to an educational organization as tuition for the education or training of such donee or (2) to a person who provides “medical care” with respect to such donee as payment for such “medical care.” These exclusions are available regardless of the relationship between the donor and the donee. Exclusions only apply to “direct payments” to the organization or person providing the qualifying services. Most importantly, these exclusions are in addition to the per donee annual exclusion amount provided in Section 2503(b) (i.e., $13,000 for 2010 and 2011). These accounts can be structured to pay qualified private school tuition, college tuition, expenses for orthodontics, and even health insurance premiums with no gift tax consequences.

2. Make loans to family members. Interest rates are historically low. The applicable federal rate (“AFR”) used to determine the adequacy of interest for non-commercial loans in November is .35% for short term (0 – 3 year) notes, 1.59% for mid-term (3+ – 9 year) notes, and 3.35% for long-term (9+ year) notes. Based upon the current rates, a taxpayer could lend $1,000,000 to a child or grandchild for three years and the required interest payments would only have to be $3,500 per year to avoid gift tax consequences.

3. Refinance existing debt. The credit markets are exceedingly tight and children and grandchildren who purchased homes under adjustable rate mortgages (ARMs) in the past may be forced to lock-in at rates that are significantly above the AFRs (see 3 above). For parents and grandparents with sufficient liquidity, it may be a perfect time to pay off existing mortgages and refinance at or above AFR rates. If properly structured and secured, interest paid still may be deductible from the income of the borrower. In addition, if pre-existing private loans are in existence, it may also be an excellent time to refinance those notes at more favorable rates.

4. Make annual exclusion gifts. The per donee annual exclusion amount provided in Section 2503(b) is for $13,000 for 2010 and remains $13,000 for 2011. While a gift tax return may be required, married couples can give up to $26,000 to a donee, or $52,000 to a donee and his/her spouse. Annual exclusion gifts can be made outright or to certain qualifying trusts.

5. Fund 529 Plans. The Code permits taxpayers to front-load 529 Plans (a.k.a., “Educational Investment Accounts”) to assist children and future generations with the increasing costs of higher education. While a transfer to a 529 Plan is a gift, so long as it and any other gifts to the beneficiary of the account in the calendar year is less than the then applicable annual exclusion amount, such transfer will not result in taxable gift. Further, an individual may pre-fund five years worth of annual exclusion gifts (currently $13,000 per year) in a single year. The end result is that a married couple filing a federal gift tax return may create a 529 Plan for a child or grandchild with an initial contribution of up to $130,000.

6. Consider Taxable Gifts in 2010. Even if a taxpayer has used all of his/her $1,000,000 lifetime exclusion for gifts, the rate for federal gift taxes is maxed out at 35% for gifts made in 2010. Unless Congress acts before year-end, the gift tax rate is scheduled to increase to 55% and the federal estate tax will be reinstated at 55% in 2011. For taxpayers so inclined to pay tax currently at a diminished rate, the positive 20% rate arbitrage between gift taxes in 2010 and 2011 should be reviewed, especially in light of the fact the generation skipping transfer (“GST”) tax, previously 55%, has a hiatus in 2010, but will come back at 55% in 2011.

7. Take advantage of broadened Roth/IRA provisions. Roth-IRAs are now available to taxpayers regardless of income level. Taxpayers may now take assets from an existing IRA, pay tax, and then transfer the assets to a Roth-IRA where the assets are permitted to grow income tax free. Roth-IRAs are not subject to the required minimum distribution rules. Taxpayers will have until October 15, 2011 to decide whether or not to “undo” the conversion and whether or not to pay all taxes with a 2010 return or to split the income taxes between 2011 and 2012 returns.

8. Transfer life insurance owned outright to an irrevocable life insurance trust (“ILIT”). By transferring life insurance policies to a properly structured ILIT, life insurance proceeds may not be includible in an insured’s gross estate for estate tax purposes, provided that he/she survives the transfer of the policies by three (3) years. The key is that the insured must give up all dominion and control over the policy. An ILIT also may be the initial owner/applicant/beneficiary of a life insurance trust without being subject to the 3-year rule. To provide the necessary liquidity to insured’s estate, the trust can purchase assets from the insured’s estate (with no adverse income tax consequences since those assets receive a new basis equal to the date of death value) at the insured’s death, or the trust can loan money to insured’s estate. Cash transferred to the ILIT to pay premiums may be structured as gifts eligible for the annual exclusion.

9. Consider gifts with discounted assets to leverage amounts of transfers. Substantial discounts for lack of marketability, minority interests and lack of control are often associated with gifts of membership interests in limited liability companies and limited partnership interests in limited partnerships. Additional “internal” discounts may be available if the entity is funded with fractional interests in real estate. Gifts in such entities may be made outright or to trusts. Although such discounts have been on the Congressional chopping block for years, recent case law substantiates the discounts where the formalities of formation, structure and operation are obeyed.

10. Fund a GRAT with appreciating assets. GRATs are still a viable entity for transferring assets to remainder beneficiaries. For a detailed discussion, see the “Planning Opportunities” discussion on page three.

Planning Opportunities in a Favorable Interest Rate Environment

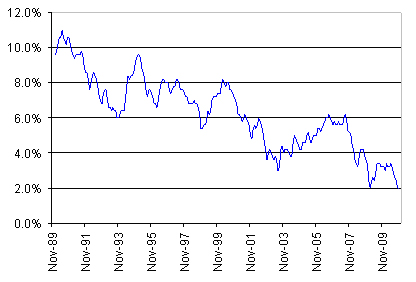

The 2010 year-end means “decision time” for many. On a personal level, deciding whether to travel for the holidays and what gifts to purchase for loved ones. From a financial planning perspective, determining whether converting a traditional IRA into a Roth IRA makes sense and/or deciding whether to make taxable gifts before December 31, 2010. In addition to these decisions, you are also presented with unique and unprecedented planning opportunities to maximize wealth transfer to children and younger generations. These opportunities are due in large part to several important factors (e.g., depressed asset value and a potentially limited timeframe to continue receiving higher valuation discounts), but perhaps most importantly are due to a favorable interest rate environment. As illustrated in Chart 1, current interest rates have dropped to historic lows.

Chart 1: Historic Section 7520 Rates

The Code Section 7520 interest rate (the “Section 7520 Rate”) is used to discount the value of annuities, life interests, and remainder interests to present value, and is revised monthly. A lower Section 7520 Rate makes certain estate planning “freeze” techniques such as grantor retained annuity trusts (GRATs) and charitable lead annuity trusts (CLATs) more attractive. The present value of the annuity payments is deducted from the fair market value of the property contributed to the trust to determine the value of the remainder interest and the resulting taxable gift.

Generally, a lower Section 7520 Rate results in a smaller taxable gift. The following table compares the Section 7520 Rate for November 2010 with the rates in November 2009 and November 2007:

Nov. 2010 Nov. 2009 Nov. 2007

Section 7520 Rate 2.0% 3.2% 5.2%

As an example, with a GRAT, assets are transferred to a trust and the grantor retains an annuity from the trust for a fixed period of time. At the end of the term, any remaining trust principal passes to the remainder beneficiaries (e.g., children) free of gift or estate tax. The GRAT will be an economic success if the assets perform well and the growth in the trust exceeds the Section 7520 Rate, with the resulting gain passing to the remainder beneficiaries. At a 5.2% Section 7520 Rate and an assumed growth rate of 7%, the required annuity payment needed to “zero out” (i.e., no taxable gift) a 10 year, $1,000,000 GRAT is $130,765 with an anticipated remainder interest of $160,442 passing to heirs. By contrast, at a 2.0% Section 7520 Rate, the required annuity payment needed to “zero out” the same GRAT is only $111,326 and the anticipated remainder interest is $429,017.

If you are philanthropically minded, a CLAT produces a similar benefit for remainder beneficiaries except that charitable organizations receive the annuity payments during the term of the trust. As with the GRAT, any growth in the CLAT in excess of the Section 7520 Rate passes to the non-charitable remainder beneficiaries with significant gift and estate tax savings.

Low AFRs - Perfect for Intra-Family Loans and Sales to Intentionally Defective Grantor Trusts

Another key interest rate, the Applicable Federal Rate (“AFR”) is used to determine the adequacy of interest for certain non-commercial loans. The Short Term AFR is used to determine the adequacy of interest for loans having a term of three years or less; the Mid Term AFR, for loans between three and nine years; and the Long Term AFR, for loans in excess of nine years. Lower AFRs make loan-based estate planning techniques, such as sales to intentionally defective grantor trusts (IDGTs) and intra-family loans, more attractive. The following table compares the AFRs for November 2010, with the rates in November 2009 and November 2007:

Nov. 2010 Nov. 2009 Nov. 2007

Short Term AFR 0.35% 0.71% 4.11%

Mid Term AFR 1.59% 2.59% 4.39%

Long Term AFR 3.35% 4.01% 4.89%

For example, you could loan $100,000 to a child or grandchild for three years and the required interest payments would only be $350 annually (assuming an interest-only balloon loan). Any growth in the funds in excess of the 0.35% Short Term AFR would remain with the child or grandchild. In contrast, the same loan three years ago would require $4,110 annual interest payments.

Additionally, now is a great time to refinance outstanding intra-family loans to lock in a lower, more favorable rate. For example, refinancing a $500,000, nine-year interest-only balloon loan made in November 2007 would cause the annual interest payment to drop from $21,950 to $7,950.

We recommend that you contact one of the members on our team if you would like to discuss any of these planning opportunities further.

Team Accomplishments and Accolades

Melissa Gray spearheaded a new volunteer program, the MVA Wills Project, with Legal Services of Southern Piedmont (LSSP). She created a drafting system for simple wills for MVA attorney volunteers to use to draft Wills for new Habitat for Humanity homeowners through the Mecklenburg County Bar and for elderly residents of Mecklenburg County. So far in 2010, MVA attorneys have assisted nearly 20 pro bono clients in completing their estate plans. Due to the success of the MVA Wills Project, Melissa and other MVA volunteer attorneys hope to continue to provide legal service to their pro bono clients.

Mark Horn has been awarded Charlotte Magazine’s Five Star Award for Best in Client Satisfaction Wealth Manager (SM) for 2010.

We are proud to announce that Wealth Transfer partner Chris Jones was recently elected as a Fellow of The American College of Trust and Estate Counsel (ACTEC). ACTEC members are elected to the College by demonstrating the highest level of integrity, commitment to the profession, competence and experience as trust and estate counselors. All ACTEC members have made substantial contributions to the field of trusts and estates law through writing, teaching and bar leadership activities.

Chris Jones spoke at the North Carolina Bar Association Estate Planning and Fiduciary Law Section Annual Meeting which took place in July in Kiawah Island, South Carolina on the topic of Recent Developments in Estate Planning and Fiduciary Law. Chris Jones also spoke at the North Carolina Bar Association 2010 Annual Review Seminar which took place in October in Greensboro, North Carolina on the same topic.

Chris Jones had an article published in both the May and September issues of the Will & The Way entitled “The Basics of U.S. Taxation of Nonresident Aliens - The Transfer Tax Aspects.”

Chris Jones and Justin Steinschriber co-authored an article entitled, “Income Tax Considerations in Structuring the Sale of S Corporation Stock to a Trust,” that was published in the July/August issue of Probate and Property.

Neill McBryde was elected as a Member of The International Academy of Estate and Trust Law. Neill McBryde was also named in Best Lawyers in America for Tax Law and Estate Law for 2011, and named in Best Lawyers in America as Trusts and Estates Lawyer of the Year in Charlotte for 2011.

Justin Steinschriber was a Co-Author of “State Conservation Income Tax Credit, An Analysis of the North Carolina and South Carolina Programs” published in The Will and the Way, a NCBA Estate Planning and Fiduciary Law Section publication. Justin Steinschriber is also a Co-Chair of the Mecklenburg County Bar Estate Planning and Probate Section.